Zhou Xiaochuan, former governor of the People’s Bank of China (PBoC), believes that digital currency and blockchain should continue to be a focus for China moving forward, citing the use of the coins for domestic retail transactions as well as remittance payments.

The PBoC’s Digital Currency Initiative

Zhou Xiaochuan, one of the most influential monetary economists in China, made his statement speaking at the 2019 Caixin Hengqin Forum on November 26, as reported by Beijing-based media outlet Caixin.

He discussed the influence that central banks across the world, PBoC included, would have in implementing central bank digital currencies (CBDCs), but was quick to emphasize that fiat currencies are “a symbol of national sovereignty” that must remain intact for any country to thrive.

Central banks, he argues, especially those of a “super sovereign power” should therefore be very cautious when choosing the direction of their blockchain and digital currency initiatives. Taking the wrong direction, he argues, could lead to a credit crisis or a lost of public trust in financial institutions.

Xiaochaun explained that the implementation of the Digital Currency Electronic Payment (DCEP) would have two primary objectives:

- An electronic payment system for use in the domestic realm.

- An international remittance use-case for inter-financial institution settlement.

Xaiochaun outlined that electronic payments and digital currencies are favorable to support the retail system in China; and once that is achieved, the use of DCEP will gradually expand into the second goal, international settlements for financial institutions.

Dovey Wan (@DoveyWan), founding parter, Primitive Capital, uses the Trojan horse as an analogy, calling the PBoC’s expansion a “land and expand” strategy:

Why the PBoC Wants It

One reason the PBoC wants a digital currency is that it make it possible for the government to track cash transactions, which officials have said would help battle money laundering, illegal gambling, and terrorist financing.

In the longer term, the People’s Bank’s digital asset could also be used to improve the efficiency of transactions across the financial system. And if many countries adopt CBDCs, this could reduce China’s exposure to US financial institutions, thus making the country less vulnerable to sanctions.

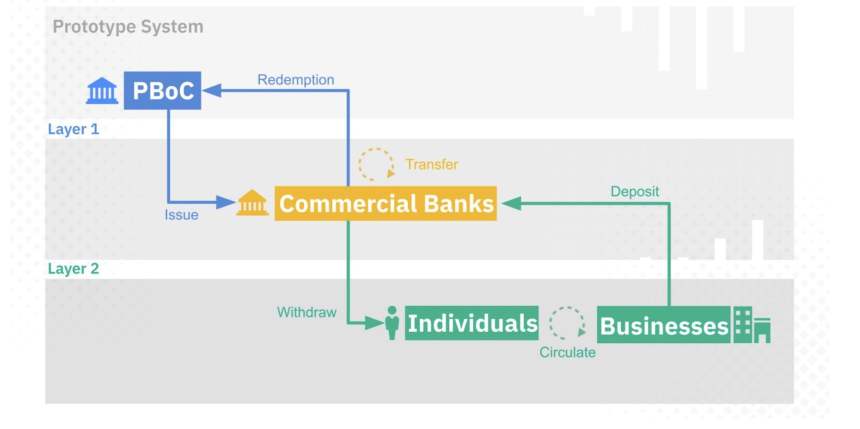

Further, if people can hold their digital coils directly at the central bank, they could cut out the middle men: retail banks. That said, as noted above, Xaiochaun doesn’t want the central bank’s digital currency to become a threat to the retail banking system.

Instead, according to the head of digital currency research for the PBoC, Mu Changchun, the currency will be issued to existing financial institutions who will distribute it for use by customers, much like fiat currency is issued now: